Doctors who have their own practice can normally qualify for many medical clinic loans because of their high earning capacity, strong net value, and stable earnings. An SBA loan will typically give a doctor the cheapest monthly payment of the majority of term loans. But, alternative small business lenders will get you funded for medical practice loans quicker and with less paperwork.

If you can not wait for the 2-3 months to get an SBA loan or do not need to manage all the paperwork, consider a short-term loan from OnDeck, that sponsored this report. OnDeck delivers prime borrowers rates as low as 6.99% and will get you financed in as fast as 1 day. Apply online for around $500K.

Visit OnDeck

Where to Get Medical Practice Financing for Physicians

Doctors usually have loads of financing options when they’re searching for cash to fund their practice. This is due to the medical field being a very safe bet for creditors, and the fact that doctors are very likely to earn enough money to cover any possible debt obligations. This means that doctors can be picky in finding medical clinic financing that fits their precise needs.

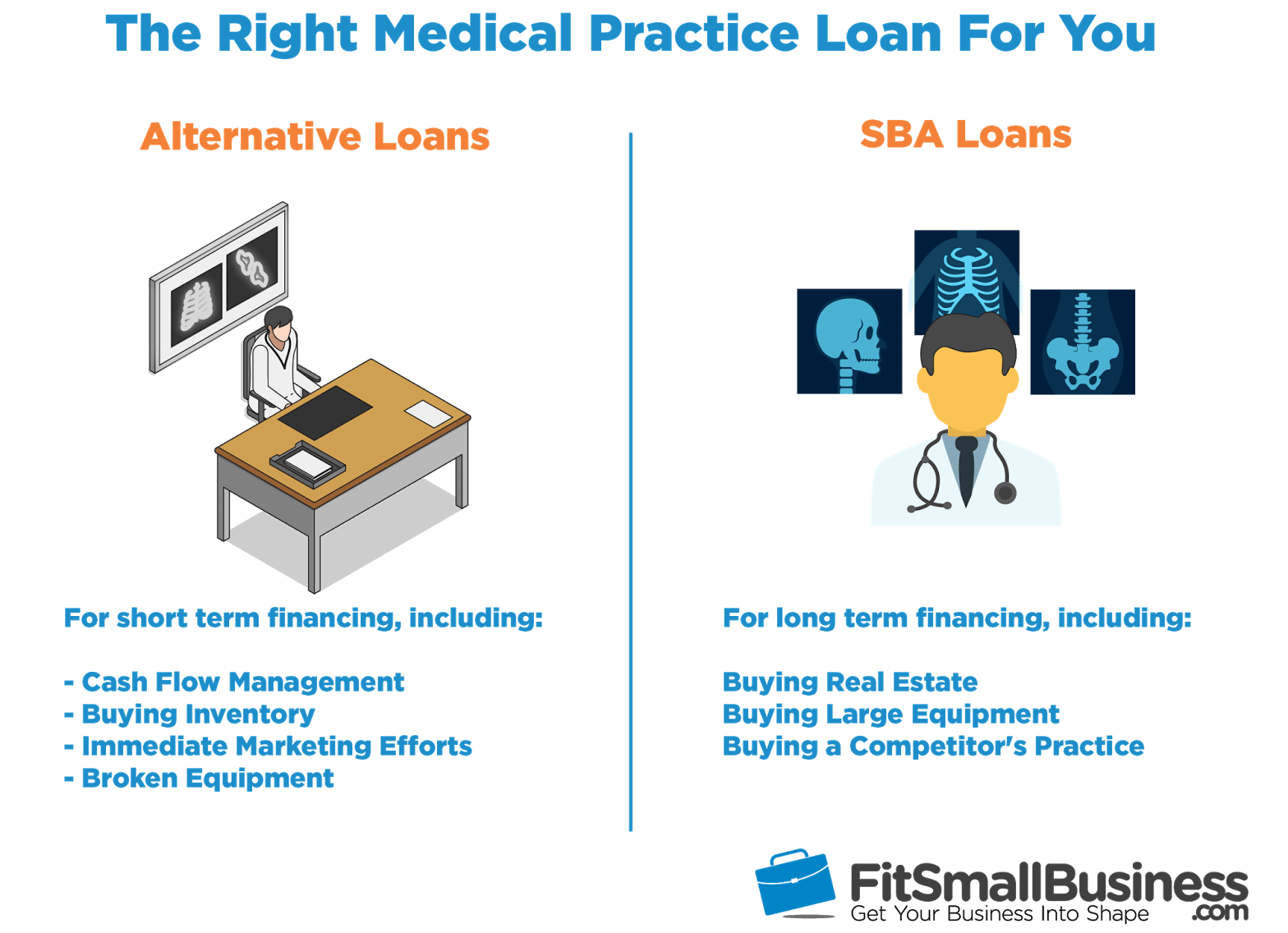

There Are Usually two main choices for medical practice funding:

1. Conventional Bank or SBA Medical Care Loan

The very best long-term financing choice is usually likely to be a loan out of the conventional lender or an SBA loan through a conventional lender. These funding options typically offer the lowest prices and longest repayment terms available. They also can take a bit longer to fund, and call for a lot more documentation than other loan choices.

These classic medical clinic loans are a fantastic option for physicians who can wait for up to 120+ days to get financed, and who are interested in finding a long-term financing solution. This makes them great if you’re buying into a private practice or if you’re funding a brand new practice and need to buy real estate or expensive equipment.

In this article, we’re going to focus on SBA loans, rather than traditional bank funding, as our long-term financing case since they are the most readily available traditional loan option for Doctors seeking to start or purchase a practice.

2. Option Loans

Another option for medical practice financing is to receive an alternative loan, which can be a short-term loan or line of credit used for immediate cash flow requirements. Such loans generally have higher rates of interest and shorter repayment conditions. This makes them a good match for short-term financing needs, like replacing inventory or paying for marketing efforts.

Doctors with a significant amount of debt may not qualify for SBA loans, maybe producing these alternative loans their only option. This is especially important to physicians looking to initiate a practice out of college because 47% of physicians have $100K+ in medical college loans. That amount of debt can make it even more difficult to qualify for an SBA loan or even a conventional bank loan.

If you only have to finance a short-term solution then these loans will probably have a smaller overall cost of capital than SBA loans. Option loans typically are only in repayment for up to 3 years, whilst SBA loans could be spread out over 10 years. Making that lots of more interest payments raises your overall cost of funds of the loan.

SBA Loans vs Choice Loans for Physicians

The two SBA loans and other loans can be helpful for physicians, based on what your objectives are, what your credit profile looks like, and also how much cash you want. SBA loans offer lower rates, longer repayment terms, and higher loan amounts. But other loans may offer fast funding (as fast as 1 day), and their rates could be comparable to SBA loans if you are a prime debtor.

Medical Practice Financing: SBA Loans vs Choice Loans

| Alternative Loan | SBA Loan | |

|---|---|---|

| Time for Initial Approval | 1 Day | 1 Week |

| Time to Receive Money | 1-3 Days | 30-120+ Days |

| Loan Amounts | $5K – $500K | $30K – $5 Million |

| Repayment Conditions | 3 Months – 3 Years | 7-10 Years |

| Average APR Range | Average of 30-50percent (As low as 6.99%) |

6-9.5percent |

| Credit Score Required | 500+ | 680+ |

| Annual Gross Revenue | $100K | $120K |

| Time in Business | 1 Year | 2 Years |

| Apply at OnDeck | Apply for an SBA Loan |

Funding Speed for Medical Practice Loans

The rate that you are financed is most important if you’ve got a direct need, such as, for instance, a cash flow issue or if an important piece of gear breaks. Option loans will fund much quicker than SBA loans. Because there are many alternative loan providers out there with varying rates & terms, we will look at only 1 provider, OnDeck.

OnDeck Funding Speed

OnDeck can normally get you financed in 2-3 business days. Should you will need the funds for a direct need, like purchasing new scopes or replenishing stock, then a fast small business loan from OnDeck could be a fantastic selection for your medical practice.

OnDeck Funding Speed at a Glance

- Prequalification: A couple of minutes

- Time for Approval: 1 Day

- Time to Get Funds: 2 — 3 Day

SBA Loan Funding Speed

The one big drawback to an SBA loan is how long it takes to both go through the application procedure and become funded. It’s typical for the procedure to take 45-120+ days from beginning to end. This makes it difficult to take advantage of the lower rates if you have time-sensitive financing needs.

Sba Medical Practice Loan Funding Speed at a Glance

- Prequalification: 1 Week

- Time for Approval: 1 — 2 Fragrant

- Time to Receive Funds: 30 — 90+ Days

Application Procedure for Medical Practice Loans

OnDeck Application Process

Applying to an OnDeck loan requires several simple personal and business information, which can be submitted completely online. OnDeck then assesses your business cash flow by syncing with your bookkeeping applications and bank account.

If convenience is important to youpersonally, OnDeck can be quite a good choice to acquire medical practice financing. OnDeck can give you up to $500K for your medical clinic without you having to go through the headaches that an SBA loan takes. Your basic personal and business information, for example bank statements, is enough info to get you approved.

OnDeck Application Process in a

- Program: Improving 100% online

- Document Collection: Complete integration with accounting applications and bank accounts is finished 100% online

- Underwriting: Automated

- Closing: 100% online plus can be done quickly (1-3 times ) after you’re approved

Visit OnDeck

SBA Loan Application Process

Finding an SBA loan will need a great deal of documentation, and your creditor will probably have a great deal of concerns for you and your business. The more complex or involved your financial position isthe longer it is very likely to take for one to get funded.

After your first application submission your SBA lender will typically need the following documents for every business you own:

- Ownership Information

- YTD Balance Sheet

- YTD P&L Statements

- Projected Financials (1-3 years)

- Business Licenses

- Business History & Overview

- All Business Leases

- Business Tax Returns (Last 2 years)

- Personal Tax Returns for all 20%+ Owners (Last 2 years)

- Resumes for all 20%+ Owners

Additionally, if you plan to purchase a different medical clinic together with the SBA loan proceeds, You’ll Be required to Supply the following advice about the medical clinic being bought:

- Buy Deal

- Present Balance Sheet

- YTD P&L Record

- Federal Tax Returns (Last two years)

- Schedule of Inventory, Equipment, Fixtures, and Other Assets

As soon as you submit all the essential documentation that your lender will underwrite the loan and request the SBA’s acceptance in order to receive the SBA guarantee. The whole procedure can easily take up to 90 days. It may take longer if you’ve got multiple legal issues for multiple medical practices, investment properties, etc..

SBA Loan Program Process in a

- Program: Often takes many trips to the bank

- Document Collection: Emailing, faxing, and turning in hard copies at a physical branch place

- Underwriting: Lots of follow up from your loan and the creditor’s underwriting team

- Closing: Requires review of 90+ pages of loan documents, if closing documents are accepted by the lender.

Medical Practice Loan Rates

With an SBA loan that you may expect to find the lowest monthly payment, however a short-term loan with a creditor such as OnDeck will probably have a lower total cost of funding. This is because you can refund the OnDeck loan within three decades, while you might be paying interest on an SBA loan for up to ten years.

Costs of an Alternative Loan From OnDeck

- Origination Fee: 5% of the total loan

- Average APR Range: 30% — 50% (rates start at 6.99percent for prime borrowers

- Repayment Terms: 3 Months — 3 Years

- Calculate Your Prices: Pre-qualify to an OnDeck loan within 5 minutes and see just how much it may cost you.

SBA Loan Costs

- Origination Fee: 0 — 4% of the Entire loan. An extra SBA guarantee fee of 3-3.5percent applies loans above $150,000

- Typical APR Range: 6 percent — 9.5percent

- Typical Repayment Conditions: 10 Years

- Calculate Your Costs: you’ll be able to use our SBA Loan Calculator to find out your potential SBA loan costs.

SBA Medical Care Loans vs Choice Loans: Minimum Qualifications

Minimum requirements for a loan won’t often function as the top concern as a physician unless you are out of medical school and have a limited income history or even a massive amount of medical debt. SBA loans will probably be more challenging to qualify for under these circumstances.

Eligibility Requirements for an OnDeck Loan

- Credit score: 500+ (check yours at no cost )

- Annual Gross Revenue: $100,000+

- Period in Business: 12+ Months

SBA Loan Qualification Requirements

- Credit Rating: 680+ (check yours for free)

- Annual Gross Revenue: $120,000+

- Period in Business: 2+ Years

Alternative loans out of OnDeck are a lot easier to qualify for than SBA loans, and they can be financed much quicker. If you have a short-term financing requirement for your medical clinic then you can apply online and prequalify in 5 minutes. OnDeck can get funded for up to $500K in as fast as 1 day. And if you are a prime borrower, your prices are often as low as 6.99%.

Visit OnDeck

That Medical Practice Loans are Ideal For You

Medical practice financing aids doctors start a new practice, buy a practice, or to expand their current practice. The nature of your company demands specialized equipment and adequate tools to satisfactorily support your patients. This can be quite costly to new or expanding practices, and medical practice financing can help you overcome those hurdles.

Physicians have many distinct applications and reasons for obtaining financing, and you should generally contemplate whether yours is a brief term or long term financing need. As an example, if you want funds to market your new practice or to replenish inventory while you wait on insurance premiums, then short-term financing is a fantastic solution.

But if your requirements are more long term then you’ll want to think about other funding options such as an SBA loan. This includes buying property or funding large equipment purchases which have a long shelf life, like x-ray machines. This will keep your instant costs low on those resources you plan to hold for a very long period of time.

Let us look at the five main reasons you are likely to get medical practice financing and which loan may be Perfect for you in each scenario:

1. Financing to Help Manage Cash Flow While Waiting on Payments

Many medical clinics, whether generalists or specialists, can occasionally run into trouble receiving timely payments for the services they supply. Due to slow donors, bounced checks, and problems with billing departments at insurance companies, even a wholesome practice with a steady flow of patients can have a tight cash flow.

Possessing the ideal financing available to help manage cash flow is critical. While it might make sense to charge some regular expenses to a small business credit card, additional expenses will require instant cash available in your business checking or savings account. By making sure payroll is met to covering your lease, it is helpful to have access to quick capital.

A good example is treating folks involved in a litigation. These kinds of treatments are generally offered in advance of payment since the bills are covered by a settlement. Court proceedings can drag on, and make it difficult to predict when you’ll be paid for your services.

A long-term loan, such as an SBA loan, is a fine instrument for this particular job. However, because it can take upwards of three months to get, you need to have it set up before your cash flow gets tight. Even though, despite that low APR, you are possibly sitting on fresh capital and getting charged interest the entire time. At the end of the day, that will greatly increase your overall cost of capital.

In that situation, a credit line might be a much better alternative. A small business line of credit is a good tool to help manage cash flow. OnDeck delivers a credit line product that has a very simple online application. You are able to get a line of up to $100K with prices as low as 13.99% in only a couple days.

Having an OnDeck line of credit you only pay interest on the amount you draw, and you’ve got 6 months to repay your balance after every draw. Having access to a credit line before you want the funds means you’re never in danger of coming up short because flaws in A/R.

Visit OnDeck

2. Acquire Another Medical Practice or to Buyout a Partner

Obtaining a competing medical clinic or buying out a partner may be a terrific way for you to grow your company. It can indicate serving new territories, offering new solutions, and obtaining new patients.

A number of these opportunities are planned out long in advance but others are caused by completely unforeseeable circumstances, such as a competitor retiring early. How long you’ve had to plan for the opportunity will have a large effect on what financing will best enable you to proceed with any chance.

In the event the purchase or buyout has been part of a strategy being developed with different partners or mentors, you will likely have time to arrange long duration, very low rate funding with an SBA loan. Even though SBA 7a loans often take 2-3 month to obtain and take a great deal of paperwork and effort during the application process, you are able to borrow up to $5 million at good rates.

However, not every single acquisition or buyout is the end result of a well planned transition. Sometimes chances present themselves quite suddenly and flaws in funding time can mean losing out to a competitor.

In such scenarios, the speed of getting funding with OnDeck is difficult to beat. The borrowing limit of $500K may restrict certain buyouts, but it should be enough to ease a transaction for most medical practices.

3. Purchase Equipment for Your Practice

Having the ideal equipment for your office is critical. Whether an important piece of equipment goes down, you are losing revenue. If you’re not buying new equipment, you’re limiting your highest revenue capabilities, and restricting the range of patients it’s possible to diagnose and treat.

If you need equipment to complete your new office, or a growth location, then you probably have sufficient time to work through the procedure and period of an SBA loan. However, if some of your expensive gear, like your x-ray system, breaks suddenly you may realize that you want funds considerably faster to protect against a loss in business.

The best approach to manage large equipment that breaks, such as an infusion pump, is using a small business line of credit on hand to get ready for these occasions. If you do not have a LOC at your fingertips, then you likely will have to access a small business loan quickly.

Along with medical gear your medical clinic is going to typically have a sizable annual expense in IT equipment and software. The HIPAA laws are extremely strict nowadays, and it’s more important than ever to keep your patient’s health data secure. You can expect to spend up to 10-12percent of your gross revenues every year just in your IT expenses.

If you have time to get ready for bigger purchases, like updating your IT software or purchasing equipment for your new office, then you might want to check in an SBA loan.

But when you have gear that breaks and you want money to replace it quickly then you probably can not wait for the 30-90 times an SBA loan generally takes to fund. In such special cases you need to visit OnDeck to see just how much you really can get financed for this particular week.

Visit OnDeck

4. Purchase Business Real Estate for Your Health Care Practice

Purchasing commercial real estate for a medical clinic is a great way for doctors to cultivate their net worth, and it might lower your monthly expense payments if you are currently renting.

“The majority of doctors do not like to lease office space. We like to view what things in our business grow in value, and leasing does not help us do that. The drawback is that our company continues to grow and we want more space, but purchasing new real estate is expensive. A long-term loan is best to help us to grow at the ideal rate and it enables us to can money in the business.”

— Dr. Vik Tarugu, owner of Detox of South Florida

When the right property place comes together to expand your business you don’t want to have to pass on it because of a scarcity of money. Much like SBA loan, most commercial real estate loans have lengthy application processes and can have a long time to finance. In case the purchase of your next office or clinic is planned far enough in advance, timing should not be an issue.

On the other hand, in case an unexpected opportunity arises and you need financing quickly, an alternate loan from OnDeck may be a good fit. Medical practice centers are typically affordable enough that short term financing could be used as a bridge loan until you can get funded for a commercial property loan with longer repayment terms.

5. Marketing & Advertising to Boost Your Medical Practice

You might need money for various marketing tasks if you want to cultivate your practice, develop a new practice, relocate, or when expanding and opening a satellite office. Marketing a health clinic is generally performed through both online and offline activities.

Online Marketing & Advertising Activities For Medical Practices

- Building a New Website

- Local Search Engine Optimization Efforts

- Paid Advertisements on Google

- Paid Promotion on Facebook

- Social Media Management

Offline Marketing & Advertising Activities For Medical Practices

- Flyers

- TV Commercials

- Billboards

- Vanity Phone Numbers

- Approaches to Gain Local Press

If your healthcare practice is quite new then you might not have the operating capital funds to present your promotion efforts what they really need to help your business grow. Getting quick access to funding from a lender such as OnDeck can get you funding when you want it so you don’t miss a growth opportunity.

Visit OnDeck

Advantages of an Alternative Loan for Medical Practices

Both long-term funding, such as SBA loans, and short-term funding, like other loans from OnDeck, can be good possibilities for physicians. Understanding when to use each is key to maximizing the value of your health care practice finances. While many will wish to wait for long-term financing to save their monthly payments, you might find the benefits of an alternate loan just as helpful.

Alternative loans for doctors have 3 Main advantages:

1. Alternative Loans are Fast & Easy

Alternative loan providers can get you financed in as little as one day. In addition they have a far more simple application procedure, letting you apply online in about five minutes. All this implies that you have more time to take care of patients, handle your medical practice, and grow your enterprise.

2. Alternatives Lenders May Take a 2nd Position

While physicians can often have their choice of funding, many traditional lenders (bank and credit unions, SBA loan suppliers, etc) will want to take a 1st place on most of collateral. This may be difficult for some physicians with multiple loans, and it might be too restrictive for others searching for a quick funding alternative. Some other creditors are comfortable taking another position to others.

3. Alternative Lenders Offer Competitive Prices for Prime Borrowers

More and more, other lenders are providing prime borrowers rates that are as competitive as most bank financing. By way of example, OnDeck offers rates as low as 6.99% to well-qualified borrowers. Should you qualify then it’s difficult to justify the additional hoops you must pass in order to get an SBA loan or to acquire other standard financing.

Bottom Line

Doctors that possess their own practice will generally have no lack of borrowing options. SBA loans, with their low rates and long repayment provisions are a very attractive option. But their protracted and involved application procedures can make SBA loans feel like a lot of work. This is particularly true once you’re juggling the day-to-day operations of your practice.

OnDeck is meeting the requirements of prime creditors, like Doctors looking for medical practice loans, all of the time. They offer speeds as low as 6.99%, make an application process which takes minutes rather than months, and may get loans approved and financed within 1-3 days. These loans are becoming more competitive with traditional financing options daily. Qualify online now for around $500K.

Visit OnDeck